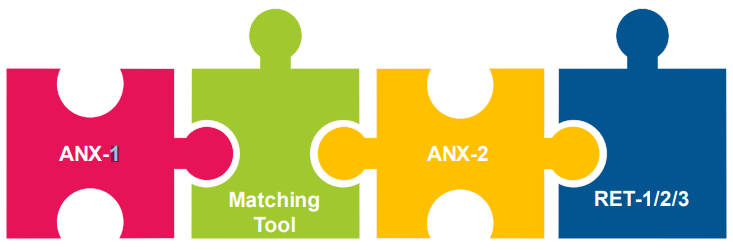

GST Council in its 31st meeting recommended introduction and implementation of a new GST Return System in a phased manner from October 2019 to facilitate taxpayers. In the new GST Return System, there will be three main components to the new return – one main return (FORM GST RET-1) and two annexures (FORM GST ANX-1 and FORM GST ANX-2). From October 2019 onwards, the current FORM GSTR-1 will be replaced by FORM GST ANX-1. e large taxpayers whose aggregate annual turnover in the previous nancial year was more than Rs. 5 Crore will upload their monthly FORM GST ANX-1 from October 2019 onwards. However, the small taxpayers whose aggregate annual turnover in the previous nancial year was upto Rs. 5 Crore will upload their rst quarterly FORM GST ANX-1 only in January 2020 for the quarter October to December 2019. Invoices, etc.,

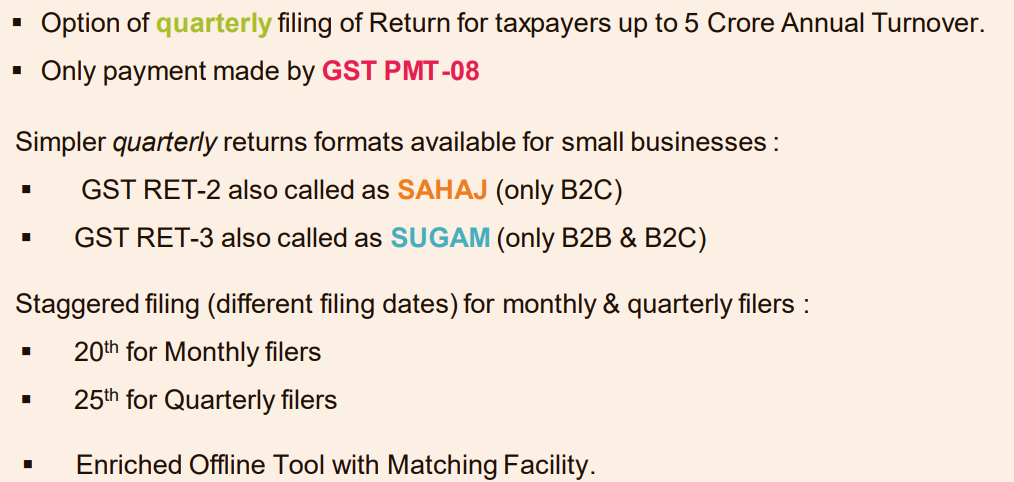

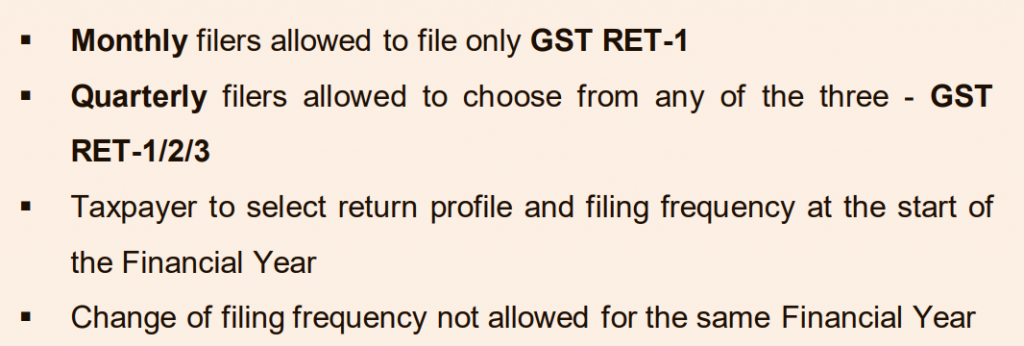

can be uploaded in FORM GST ANX-1 on a continuous basis both by large and small taxpayers from October 2019 onwards. For October and November, 2019, large taxpayers will continue to le FORM GSTR-3B on monthly basis. ey will le their rst FORM GST RET-1 for the month of December 2019 by 20th January 2020. e small taxpayers opting to le FORM GST RET-1 on a quarterly basis will stop ling FORM GSTR-3B and will start ling FORM GST PMT-08 from October 2019 onwards. ey will le their rst FORM GST-RET-1 for the quarter October 2019 to December 2019 by 20th January 2020. e periodicity of ling return in FORM GST RET-1 will be deemed to be monthly for all taxpayers unless quarterly ling of the return is explicitly opted for by small taxpayers. e aggregate annual turnover of newly registered taxpayers will be considered as zero and they will have the option to le a quarterly return. In addition, small taxpayers can choose to le, instead of FORM GST RET-1, any of the other two new quarterly returns, namely, Sahaj (FORM GST RET- 2) and Sugam (FORM GST RET-3). Small taxpayers opting to le the return on quarterly basis are required to pay tax, either by cash or credit or both, on monthly basis on the taxable supplies made during the month by ling FORM GST PMT – 08 for the rst two months of the quarter. Tax must be paid by 20th of the month succeeding the month which the tax liability pertains to. Taxpayers whose aggregate turnover in the preceding nancial year was above Rs.5 Crore will have to le monthly return. is return needs to be led monthly by 20th of the month succeeding the month to which the tax liability pertains.

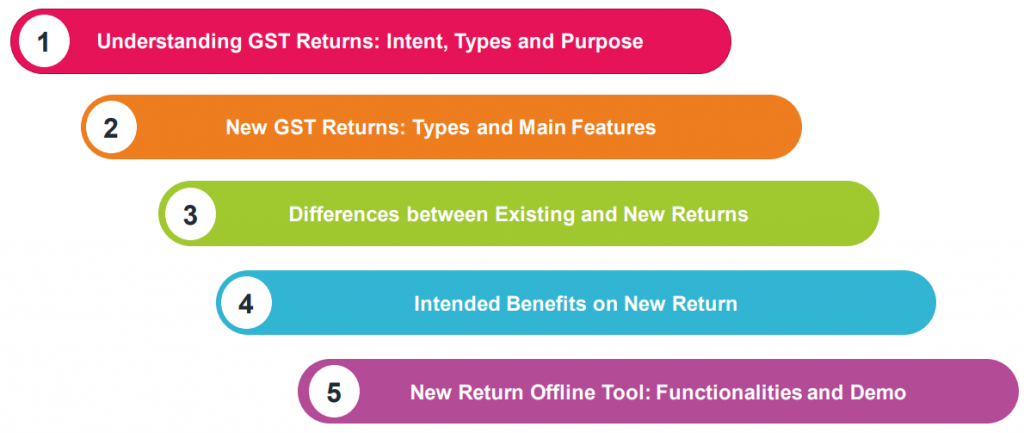

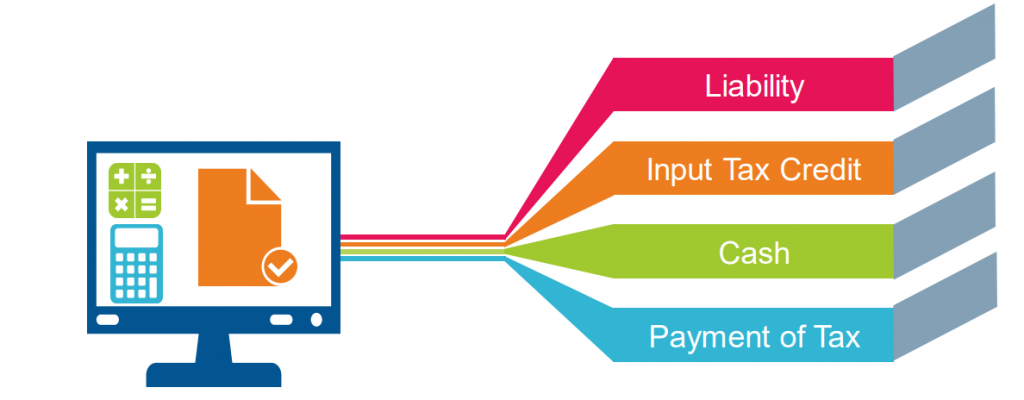

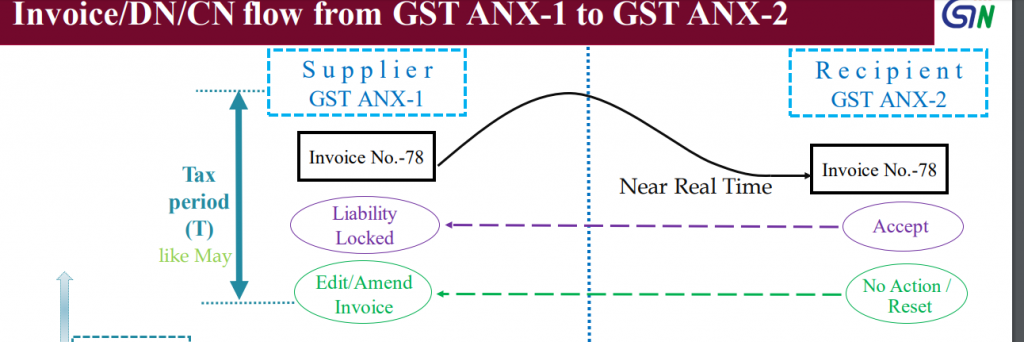

Monthly return in FORM GST RET-1 needs to be led based on FORM GST ANX – 1 and FORM GST ANX – 2 . Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore can le this return. is return needs to be led quarterly by 20th of the month succeeding the quarter to which the tax liability pertains. Tax has to be paid on monthly basis through FORM GST PMT-08. Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore and have supplies only to consumers and unregistered persons (B2C supplies) can le this return based on FORM GST ANX – 1 and FORM GST ANX – 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08. Taxpayers opting to le Sahaj can declare outward supply under B2C category and inward supplies a racting reverse charge only. E-commerce operators are ineligible to le Sahaj. Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore and have made supplies to consumers and un-registered persons (B2C) and to registered persons (B2B) can le this return based on FORM GST ANX – 1 and FORM GST ANX – 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08. Taxpayers opting to le Sugam can declare outward supply under B2C and B2B category and inward supplies a racting reverse charge only. E-commerce operators are ineligible to le Sugam. Salient features of the New GST Return System Option to le quarterly return is available for taxpayers whose aggregate annual turnover in the previous nancial year was upto Rs. 5 Crore. Option to le NIL return through SMS. Invoice details can be uploaded by the supplier and the same can be viewed by the recipient on real time basis. Matching tool is available which will help the taxpayer to match their Input Tax Credit based on their FORM GST ANX – 2 and purchase register. New GST Returns FORM GST RET-1 (Normal Monthly) FORM GST RET-1 (Normal Quarterly) FORM GST RET-2 (SAHAJ Quarterly) FORM GST RET-3 (SUGAM Quarterly) Back

e GST Council in its 31st meeting recommended introduction and implementation of a new GST Return System in a phased manner from October 2019 to facilitate taxpayers. In the new GST Return System, there will be three main components to the new return – one main return (FORM GST RET-1) and two annexures (FORM GST ANX-1 and FORM GST ANX-2). From October 2019 onwards, the current FORM GSTR-1 will be replaced by FORM GST ANX-1. e large taxpayers whose aggregate annual turnover in the previous nancial year was more than Rs. 5 Crore will upload their monthly FORM GST ANX-1 from October 2019 onwards. However, the small taxpayers whose aggregate annual turnover in the previous nancial year was upto Rs. 5 Crore will upload their rst quarterly FORM GST ANX-1 only in January 2020 for the quarter October to December 2019. Invoices, etc., can be uploaded in FORM GST ANX-1 on a continuous basis both by large and small taxpayers from October 2019 onwards. For October and November, 2019, large taxpayers will continue to le FORM GSTR-3B on monthly basis. ey will le their rst FORM GST RET-1 for the month of December 2019 by 20th January 2020. e small taxpayers opting to le FORM GST RET-1 on a quarterly basis will stop ling FORM GSTR-3B and will start ling FORM GST PMT-08 from October 2019 onwards. ey will le their rst FORM GST-RET-1 for the quarter October 2019 to December 2019 by 20th January 2020. e periodicity of ling return in FORM GST RET-1 will be deemed to be monthly for all taxpayers unless quarterly ling of the return is explicitly opted for by small taxpayers. e aggregate annual turnover of newly registered taxpayers will be considered as zero and they will have the option to le a quarterly return. In addition, small taxpayers can choose to le, instead of FORM GST RET-1, any of the other two new quarterly returns, namely, Sahaj (FORM GST RET- 2) and Sugam (FORM GST RET-3). Small taxpayers opting to le the return on quarterly basis are required to pay tax, either by cash or credit or both, on monthly basis on the taxable supplies made during the month by ling FORM GST PMT – 08 for the rst two months of the quarter. Tax must be paid by 20th of the month succeeding the month which the tax liability pertains to. Taxpayers whose aggregate turnover in the preceding nancial year was above Rs.5 Crore will have to le monthly return. is return needs to be led monthly by 20th of the month succeeding the month to which the tax liability pertains. Monthly return in FORM GST RET-1 needs to be led based on FORM GST ANX – 1 and FORM GST ANX – 2 . Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore can le this return. is return needs to be led quarterly by 20th of the month succeeding the quarter to which the tax liability pertains. Tax has to be paid on monthly basis through FORM GST PMT-08. Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore and have supplies only to consumers and unregistered persons (B2C supplies) can le this return based on FORM GST ANX – 1 and FORM GST ANX – 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08. Taxpayers opting to le Sahaj can declare outward supply under B2C category and inward supplies a racting reverse charge only. E-commerce operators are ineligible to le Sahaj. Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore and have made supplies to consumers and un-registered persons (B2C) and to registered persons (B2B) can le this return based on FORM GST ANX – 1 and FORM GST ANX – 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08. Taxpayers opting to le Sugam can declare outward supply under B2C and B2B category and inward supplies a racting reverse charge only. E-commerce operators are ineligible to le Sugam. Salient features of the New GST Return System Option to le quarterly return is available for taxpayers whose aggregate annual turnover in the previous nancial year was upto Rs. 5 Crore. Option to le NIL return through SMS. Invoice details can be uploaded by the supplier and the same can be viewed by the recipient on real time basis. Matching tool is available which will help the taxpayer to match their Input Tax Credit based on their FORM GST ANX – 2 and purchase register. New GST Returns FORM GST RET-1 (Normal Monthly) FORM GST RET-1 (Normal Quarterly) FORM GST RET-2 (SAHAJ Quarterly) FORM GST RET-3 (SUGAM Quarterly)

Back e GST Council in its 31st meeting recommended introduction and implementation of a new GST Return System in a phased manner from October 2019 to facilitate taxpayers. In the new GST Return System, there will be three main components to the new return – one main return (FORM GST RET-1) and two annexures (FORM GST ANX-1 and FORM GST ANX-2). From October 2019 onwards, the current FORM GSTR-1 will be replaced by FORM GST ANX-1. e large taxpayers whose aggregate annual turnover in the previous nancial year was more than Rs. 5 Crore will upload their monthly FORM GST ANX-1 from October 2019 onwards. However, the small taxpayers whose aggregate annual turnover in the previous nancial year was upto Rs. 5 Crore will upload their rst quarterly FORM GST ANX-1 only in January 2020 for the quarter October to December 2019. Invoices, etc., can be uploaded in FORM GST ANX-1 on a continuous basis both by large and small taxpayers from October 2019 onwards. For October and November, 2019, large taxpayers will continue to le FORM GSTR-3B on monthly basis. ey will le their rst FORM GST RET-1 for the month of December 2019 by 20th January 2020. e small taxpayers opting to le FORM GST RET-1 on a quarterly basis will stop ling FORM GSTR-3B and will start ling FORM GST PMT-08 from October 2019 onwards. ey will le their rst FORM GST-RET-1 for the quarter October 2019 to December 2019 by 20th January 2020. e periodicity of ling return in FORM GST RET-1 will be deemed to be monthly for all taxpayers unless quarterly ling of the return is explicitly opted for by small taxpayers. e aggregate annual turnover of newly registered taxpayers will be considered as zero and they will have the option to le a quarterly return. In addition, small taxpayers can choose to le, instead of FORM GST RET-1, any of the other two new quarterly returns, namely, Sahaj (FORM GST RET- 2) and Sugam (FORM GST RET-3). Small taxpayers

opting to le the return on quarterly basis are required to pay tax, either by cash or credit or both, on monthly basis on the taxable supplies made during the month by ling FORM GST PMT – 08 for the rst two months of the quarter. Tax must be paid by 20th of the month succeeding the month which the tax liability pertains to. Taxpayers whose aggregate turnover in the preceding nancial year was above Rs.5 Crore will have to le monthly return. is return needs to be led monthly by 20th of the month succeeding the month to which the tax liability pertains. Monthly return in FORM GST RET-1 needs to be led based on FORM GST ANX – 1 and FORM GST ANX – 2 . Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore can le this return. is return needs to be led quarterly by 20th of the month succeeding the quarter to which the tax liability pertains. Tax has to be paid on monthly basis through FORM GST PMT-08. Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore and have supplies only to consumers and unregistered persons (B2C supplies) can le this return based on FORM GST ANX – 1 and FORM GST ANX – 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08. Taxpayers opting to le Sahaj can declare outward supply under B2C category and inward supplies a racting reverse charge only. E-commerce operators are ineligible to le Sahaj. Taxpayers whose aggregate turnover in the preceding nancial year was upto Rs.5 Crore and have made supplies to consumers and un-registered persons (B2C) and to registered persons (B2B) can le this return based on FORM GST ANX – 1 and FORM GST ANX – 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08. Taxpayers opting to le Sugam can declare outward supply under B2C and B2B category and inward supplies a racting reverse charge only. E-commerce operators are ineligible to le Sugam. Salient features of the New GST Return System Option to le quarterly return is available for taxpayers whose aggregate annual turnover in the previous nancial year was upto Rs. 5 Crore.